The below post is taken from the Video Blog, the Subject Matter Minute. You can view the episode on YouTube if you would like. Find it here: Episode #75 – Prudential Voluntary Life Insurance

If YouTube is blocked for you or your agency, you can scroll to the bottom of this post to view it from Google Drive. (I would prefer you view it on YouTube, so I know how many people have watched)

You can also listen to an audio version.

Hello everyone, and welcome back to the Subject Matter Minute.

I promise that this is the last time I will talk about my hip. There are a couple things I meant to share with you, but forgot. 🙂 When I was talking with my surgeon before the procedure, I was thinking it would be cool to keep the ball that they hack off the top of my femur. I had heard from a neighbor that a friend of his had kept his and used it as the top of a cane. Sounded like a cool project, so I asked. The doc smiled and said that this wasn’t allowed in Colorado. He said he thought it was a good idea too and that he had fought for it, but failed. Then he smiled and said, “so I just take them home and feed them to my dog.” We both got a good laugh out of that!

Finally, I think that the final product looks really cool, so I wanted to show you the x-ray. Check it out. I figure when I die, and I get cremated, my kids will have a really sweet weapon. I mean, look at that thing!

Ok, that’s IT for the hip.

Today we’re taking a look at a benefit that may sound familiar — because it is familiar — but with one little update: the Voluntary Life Insurance Plan through Prudential. (music)

This benefit has been available to Wyoming Retirement members for years, but after a short pause, it’s being reintroduced with one important change. I’ll explain that in just a moment.

This is a voluntary life insurance benefit available to all active WRS contributing members.

It’s issued by Prudential, administered by an outfit called Member Benefits, and available through the National Conference on Public Employee Retirement Systems — or NCPERS. Not an important detail, but dems the facts. 🙂

The plan is designed to give you guaranteed-issue life insurance, which means:

- No medical exams

- No health questions

- And you cannot lose coverage because of age or health changes

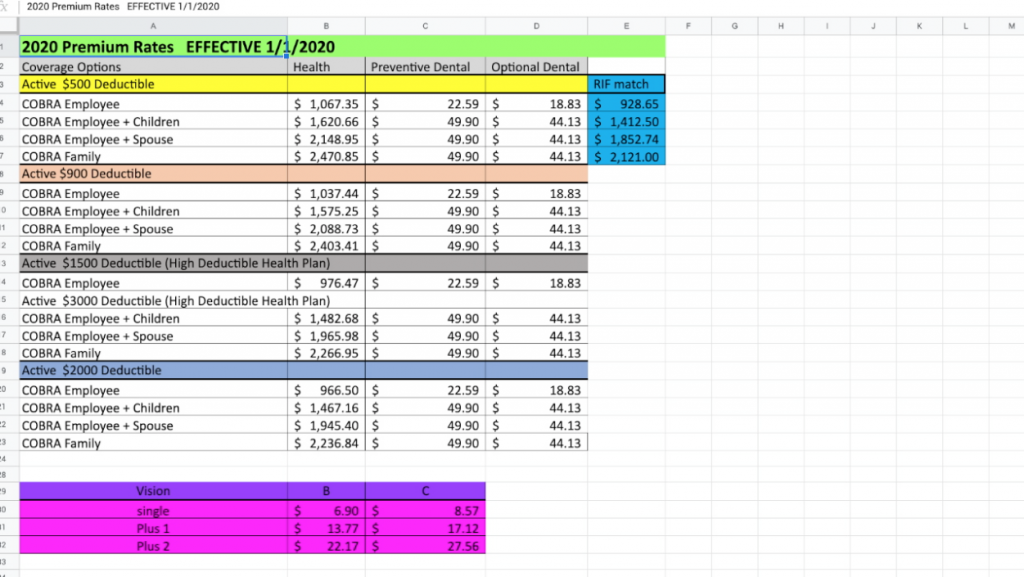

Payouts start at a higher amount when you’re younger (when debt and such tends to be greater) and gradually decreases as you age — but the premiums stay the same the whole time.

The cost is a flat $16 per month — it never increases, regardless of your age.

That $16 includes:

- Group Decreasing Term Life Insurance (Show coverage chart)

Depending on your age at the time of claim, the benefit ranges from $225,000 (When you are under age 25) down to $7,500 (for those of you age 65+).

- Accidental Death & Dismemberment (AD&D)

This adds up to $100,000 more for accidental death for most age brackets.

- Coverage for your spouse/domestic partner and dependent children

Spousal coverage varies by your age, up to $20,000, and dependent children are covered for $4,000.

- Student Loan Protection Benefit

If you’re 45 or younger, and you become totally disabled with an outstanding student loan balance, Prudential may reimburse up to $50,000.

Ok, so what has changed?

This is the part that’s new:

If you enroll going forward, you’ll pay premiums by either:

- Monthly automatic bank draft, or

- Annual direct bill

So, you can’t do payroll deduction.

If you already have this coverage from before August 2024, nothing changes — your premiums will continue through payroll deduction, just like before.

Everything else about the plan stays the same — same price, same coverage structure, same benefits.

So, who can enroll and when?

All active Wyoming Retirement contributing members can enroll:

- Within 90 days of your hire date, or

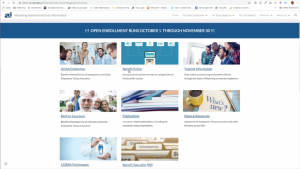

- During Open Enrollment, every year from October 1 through November 30.

If you enroll during either of these windows, your coverage begins on the first day of the month following your first payment.

There are a few other features that are worth mentioning with this program:

- If you become totally disabled before age 60, premiums may be waived.

- You may access up to 50% of your benefit if you’re diagnosed as terminally ill.

- And finally, coverage can continue into retirement. As long as you’re insured as an active member and keep receiving benefits through WRS, you can simply have premiums deducted from your retirement check.

Now keep in mind that the benefit is only $7500 when you turn 65, so it’s up to you to decide if it’s worth continuing to pay for that or not.

Alright, so how do you enroll…

You’ll need to complete an enrollment and beneficiary form:

From this page, you can learn more about the plan by clicking on “Plan Details,” or you can complete the enrollment form online by clicking “Apply Now.”

For questions, Member Benefits can be reached at 800-525-8056 or NCPERS@memberbenefits.com.

Remember, this plan is guaranteed-issue, so no one is going to ask about your missing parts or your future plans for getting a titanium weapon installed in your body. Whether you’re looking for AD&D coverage or just want to make sure your kids inherit something more valuable than a surgical-grade dagger, check out the links below. See you next time!