The below post is taken from the Video Blog, the Subject Matter Minute. If it’s a little hard to read, it’s because it’s taken from the spoken word. You can view the episode on YouTube if you would like. Find it here: Episode #56 – Pre-Retirement Checklist

If YouTube is blocked for you or your agency, you can scroll to the bottom of this post to view it from Google Drive. (I would prefer you view it on YouTube, so I know how many people have watched)

You can also listen to an audio version.

My last episode was on the upcoming raises. Well, you should all now know how much you got. I’m really hoping all of you fabulous, hard-working state employees were pleasantly surprised with what you got. I had low expectations, so that helped. (giggle) But I was pleasantly surprised. Now let’s cross our fingers that there is more money in the next couple of years to add to that and get us closer to the mid-point of our pay grades. Remember that even though it hurts, high gas prices can be good for state employees!

Alright, before I get started, I want to give a shout-out to a couple of state employees that I met at the Laramie Brewfest during Jubilee Days. Hello to Lisa of DFS and Tasha of Game and Fish. You guys are a hoot! My wife and I had a great time drinking with ya and cracking ourselves up! Am I right??

Ok, let’s get down to business. We’ve all heard the expression, “the great resignation,” right? You might even be sick of it right now, but…. Apparently, a ton of people are getting out of the game. And while right now, due to the state of the stock market, might not be the best time, if you are ready and thinking about it, WRS has a pre-retirement checklist to help you get there. …and I’m very envious of you.

Before I hit that checklist, I want to hit a couple of items that are the same, both for folks that are retiring and folks that are just moving on to another employer. Of course, we hope that never happens, but we realize it’s going to happen from time to time. First of all, whether you are retiring or just moving on, know that HR will be in touch. Not only because I’m sure there are probably a few things you need to return, but because they also want to hear from you. In fact, most will conduct what’s referred to as an exit interview – this is your chance to be honest with HR about why you are leaving. Regardless, along with an exit interview, there are a couple of items in the Personnel Rules and the Compensation Policy that pertain to retiring.

Chapter 11 of the personnel rules, which covers separation, goes over notification procedure, rescinding notification, and failure to notify. So first of all, when you decide that you are leaving the state and/or retiring, you need to provide written notification to your supervisor specifying the date and time of your resignation. Of course, you want to do it as far ahead as possible, and the rules mention that if you notify with less than 2 weeks, without good reason, you will not separate in good standing. This only matters if you want to go back to work at the state. Still, it’s kinda rude to give less than two weeks’ notice. Also, if you change your mind before the resignation date that you set, you can change it with the approval of the agency head. So if you are getting cold feet, or the stock market is doing even worse, you can push it back. 🙂

The Compensation policy goes over how you will be paid for the leave you have accumulated when you retire. First of all, you will be paid for all of your annual leave… at your hourly rate. For sick leave, you will be paid for 50% of what you have, but only up to 480 hours. So if you have an ungodly amount of sick leave, you are still only going to get a max of 480 hours.

Longevity pay is an interesting one. First of all, you will get longevity pay for the month that you quit/retire no matter how many days you work that month. So, you work 2 days, you get your longevity pay for that month. Second, you also may get what’s referred to as a Longevity Payout. This combines your annual and sick leave paid out and applies the number of hours as if they were hours worked. So… if your annual and sick leave balances add up to an equivalent of a month’s time, or several months, you will get longevity pay for each of those months.

Also, you will get paid for any comp time you have remaining.

An exempt employee will get paid for any unused Paid Time Off.

And finally, if you have any other type of leave accrued, use it before you leave or retire. You will lose those hours. So, leave like wellness, personal, or admin leave.

And one little fun tidbit here… if you get paid out for your annual and sick leave and then decide you can’t stand retirement and get rehired within 31 days of your retirement, you will have to pay all that money back. So…… don’t do that.

Ok… so that covers the personnel rules and compensation part of retiring. Now let’s hit this checklist that WRS puts out. It’s approximately 8 things to do before you reach your retirement date.

At 6 to 8 months from retiring, you need to request an estimate of your pension benefits. You can do that on the website or you can give them a call. Now, if you are planning to retire on the “earliest date for unreduced retirement benefits” then WRS says you need to contact a Benefits Specialist for final verification of the Rule of 85 date within 3 months prior to terminating your job. … just to make sure you got it right. You can find your earliest date for unreduced retirement benefits at the bottom of page 1 of your statement.

Next… if you are planning to keep the state insurance, health and dental, through EGI, then you need to contact EGI 3 months out from retiring.

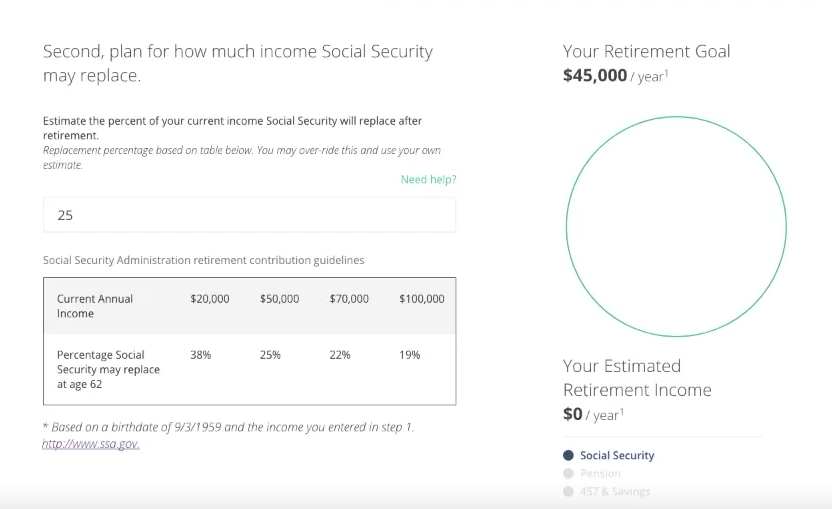

You should also consider social security and medicare. If you are eligible for social security benefits and want to start receiving them when you retire, apply approximately 3 months before. Go to www.ssa.gov or contact your local Social Security office to do this. If you are Medicare age eligible and wish to apply for Medicare, those benefits can also be applied for at: www.ssa.gov. (Click on Menu at the top and click Medicare under the Benefits section).

There is another option for your annual and sick leave benefits. You can defer them into your 457 deferred compensation plan. If you decide to do this, after careful consideration, a completed final Deferral Authorization of Accrued Leave Payouts Form must be submitted to WRS the month before your last working day. The form is on the WRS website.

Speaking of the 457 Deferred Comp plan… you should think about this account as well. Everyone should at least have a little bit in there as they match $20 a month… right? Ok, well, first of all, you don’t have to do anything with it right away. But if you do want to start withdrawing funds, go ahead and contact WRS about it. And just so you know, you will be required to start taking distributions from your 457 account in the calendar year that you turn 72.

And finally… 2-3 weeks before retiring, you can submit your pension application. Please make sure that your termination date is submitted and set before you do this. You may submit your pension application by logging into your pension account or by printing off the pension application from the website.

If you are getting close to retirement, first of all, I envy you sooooo much. But secondly, there are a ton of things to consider! Hopefully, this gives you an idea of the state-related things that you need to think about. But, no matter what, I would get on the phone with WRS to make sure you are checking all the boxes.

Alright… thanks for watching! Keep enjoying this fabulous summer and I’ll see you next time!